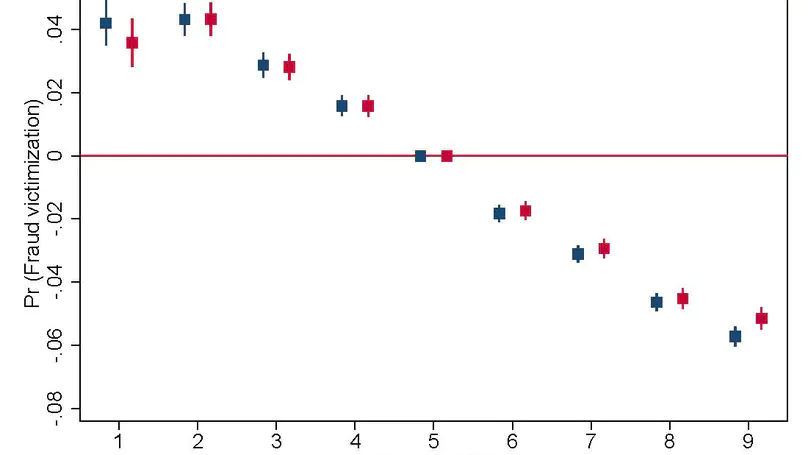

Using administrative data on individual PP fund choices matched with military enlistment intelligence test scores, we find that intelligence is strongly, negatively and almost linearly associated with investing in any of these companies. Intelligence is also strongly positively associated with the probability of divesting from these firms after, but not before, the fraud has been publicly revealed. Thus, intelligence protects against being financially victimized and it is people of low intelligence that suffer the most, which will translate into widening socioeconomic gaps in retirement along lines of intelligence.